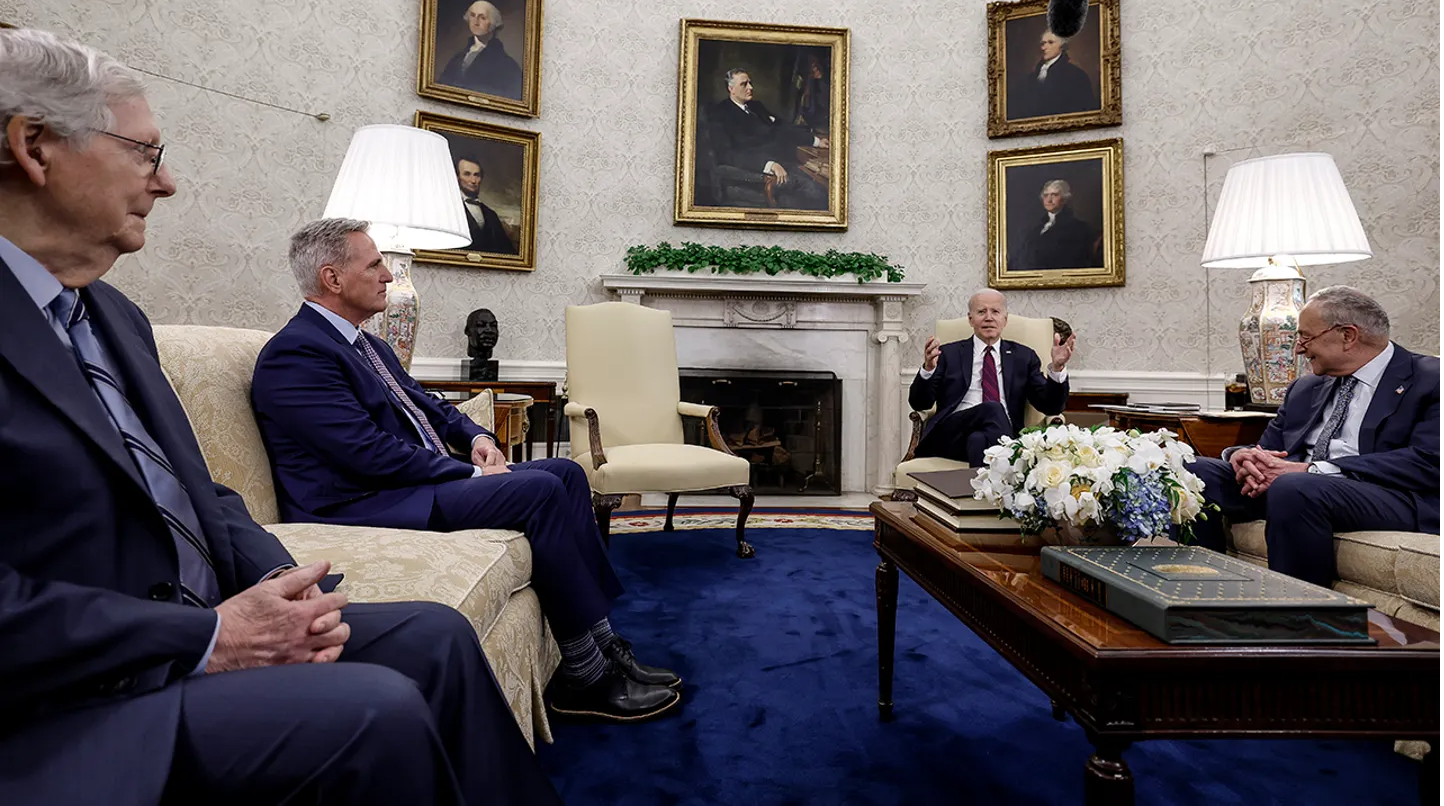

After weeks of back-and-forth, President Joe Biden and Republican House Speaker Kevin McCarthy struck a bipartisan deal to raise the debt ceiling in exchange for a series of spending cuts – including paring back funding for the Internal Revenue Service.

The IRS received an influx of $80 billion last year as part of Democrats’ health care and climate change spending bill – dubbed the Inflation Reduction Act – that Biden signed into law in August 2022.

The funding was aimed at improving tax compliance among big corporations and wealthy Americans and shrinking the estimated $600 billion tax gap.

But cuts to IRS funding are now a key component of the tentative agreement reached by McCarthy and Biden on Sunday evening.

In exchange for a two-year suspension of the debt ceiling, Republicans demanded an immediate $1.38 billion cut to the IRS. On top of that, the bill would take back up to $10 billion in each of the next two years.

“Do you know how much [Democrats are] going to spend this year for IRS agents? $1.9 billion,” McCarthy said during an interview on “Fox News on Sunday. “So, we repealed every single dollar they were going to use for IRS agents.”

The IRS – which had about 78,700 employees as of 2021 – previously said that it planned to hire nearly 30,000 new employees by the end of fiscal year 2025, including 8,782 hires in enforcement and 13,883 in taxpayer services. The new enforcement employees would be “exclusively” focused on high-earning households, larger partnerships and companies, according to IRS Commissioner Daniel Werfel.

The funding boost elicited fierce pushback from Republicans and other critics who warned that a beefed-up IRS could ultimately hurt lower-income Americans.

White House officials said the clawback in funding will not hurt near-term tax collection.

The debt ceiling, which is currently around $31.4 trillion, is the legal limit on the total amount of debt that the federal government can borrow on behalf of the public, including Social Security and Medicare benefits, military salaries and tax refunds. In a worst-case scenario, the U.S. would be so cash-strapped that it would have to delay its payment of interest or principal on the nation’s debt.

The U.S. government bumped up against that limit in January, prompting the Treasury Department to initiate a series of actions that are known as “extraordinary” measures intended to stave off a default.

Treasury Secretary Janet Yellen warned last week the country could run out of money as early as June 5 if legislators do not raise or suspend the nation’s borrowing limit.

Lawmakers are set to vote on the McCarthy-Biden agreement this week.

If the U.S. fails to raise or suspend the debt limit, it would eventually have to temporarily default on some of its obligations, which could have serious negative economic implications. Interest rates would likely spike and demand for Treasuries would drop; even the threat of default can cause borrowing costs to increase, according to the Committee for a Responsible Federal Budget.

While the U.S. has never defaulted on its debt before, it came close in 2011 when House Republicans refused to pass a debt-ceiling increase, prompting rating agency Standard & Poor’s to downgrade the U.S. debt rating one notch.